Quick. Predictable. Stress-Free.

The Lies, Misrepresentations, and Withholds Rampant within The"Business Credit" Industry

The business funding world is a minefield of misdirection. Every deceptive operator "out there" falls into one of three categories—and all of them rely on the same thing:

You not knowing the real differences between personal and business credit products.

You not knowing how banks define “credit line.”

You not knowing how underwriting software evaluates your profile.

This is where the confusion ends....This is the full exposé.

"Imposter" Business Credit

These are lenders who pretend they offer “business credit”—but everything actually reports to your PERSONAL profile.

Lenders disguising personal-reporting credit cards as “business credit.”

How They Deceive Borrowers

They hide the fact that their “business” cards report to your personal credit profile, tanking your utilization, risk, and future approval metrics.

Market their products as “business credit” while quietly reporting balances to your personal credit utilization.

They never disclose that balances will sabotage your personal borrower profile and make bank approvals nearly impossible.

What They Count On You NOT Knowing

That true BANK credit lines and loans always require a personal guarantee after the 2008 collapse—because banks now demand full-credit-risk accountability.

That true BANK credit lines always require a personal guarantee after the 2008 collapse—because banks now demand full-credit-risk accountability.

That credit cards reporting to your personal profile are approval killers, not business tools.

You don’t realize that carrying balances tanks your FICO® profile—making true bank lines impossible.

That some “business” cards are actually PERSONAL cards (Discover IT, Capital One Spark)—and these imposters poison your fundability.

That carrying balances damages your capacity for real credit lines because banks view them as high-risk behavior.

That personal “available credit” increases can actually LOWER future approval potential.

You won’t discover until too late that these accounts never graduate into real banking relationships.

What You Actually Get

Misrepresented products disguised as “business financing”

Sky-high utilization penalties on your personal profile

Lower FICO® scores

Approval-readiness downgrades

No banking relationship leverage

A dead-end credit instrument with no graduation path

Credit Card/Capital "Stackers"

These are companies that promise “business funding”—but their entire model is stacking personal and/or business credit cards.

These lenders intentionally blur the distinction between “credit card” and “credit line”—because the moment you understand the difference, you'll likely avoid their products.

How They Deceive Borrowers

They call their credit limits “credit lines” to piggyback on bank terminology—knowing you’ll assume they mean true BANK lines of credit.

Know you want bank money—but give you credit cards disguised as “business financing.”

They hide the fact that their “business” cards report to your personal credit profile, tanking your utilization, risk, and future approval metrics.

Pretend these accounts build business credit, while knowing they harm your personal borrower profile.

They rely on the loophole that they can legally label credit cards as “lines of credit”—but ethically it is pure misrepresentation.

They never disclose that balances will sabotage your personal borrower profile and make bank approvals nearly impossible.

What They Count On You NOT Knowing

That true BANK credit lines always require a personal guarantee after the 2008 collapse—because banks now demand full-credit-risk accountability.

You’ll believe their “business credit” card means that it won't report to your personal profile—even when it will.

That credit cards reporting to your personal profile are approval killers, not business tools.

That some “business” cards are actually PERSONAL cards (Discover IT, Capital One Spark)—and these imposters poison your fundability.

That carrying balances damages your capacity for real credit lines because banks view them as high-risk behavior.

Personal reporting accounts that damage your approval metrics

You won’t discover until too late that these accounts never graduate into real banking relationships.

No pathway to low-cost working capital

What You Actually Get

Misrepresented products disguised as “business financing”

Sky-high utilization penalties on your personal profile

Lower FICO® scores

Approval-readiness downgrades

No banking relationship leverage

A dead-end credit instrument with no graduation path

Business Credit "Builders"

These are companies selling the “Pay us and we help you build business credit” fantasy.

These lenders intentionally blur the distinction between “credit card” and “credit line”—because the moment you understand the difference, you'll likely avoid their products.

How They Deceive Borrowers

They call their credit limits “credit lines” to piggyback on bank terminology—knowing you’ll assume they mean true BANK lines of credit.

Know you want bank money—but give you credit cards disguised as “business financing.”

They hide the fact that their “business” cards report to your personal credit profile, tanking your utilization, risk, and future approval metrics.

They rely on the loophole that they can legally label credit cards as “lines of credit”—but ethically it is pure misrepresentation.

They never disclose that balances will sabotage your personal borrower profile and make bank approvals nearly impossible.

What They Count On You NOT Knowing

That true BANK credit lines always require a personal guarantee after the 2008 collapse—because banks now demand full-credit-risk accountability.

That credit cards reporting to your personal profile are approval killers, not business tools.

That some “business” cards are actually PERSONAL cards (Discover IT, Capital One Spark)—and these imposters poison your fundability.

That carrying balances damages your capacity for real credit lines because banks view them as high-risk behavior.

That personal “available credit” increases can actually LOWER future approval potential.

What You Actually Get

Misrepresented products disguised as “business financing”

Sky-high utilization penalties on your personal profile

Lower FICO® scores

Approval-readiness downgrades

No banking relationship leverage

A dead-end credit instrument with no graduation path

False sense of business credit progress

What Get Fundable! Offers...

These are companies selling the “Pay us and we help you build business credit” fantasy.

These lenders intentionally blur the distinction between “credit card” and “credit line”—because the moment you understand the difference, you'll likely avoid their products.

How They Deceive Borrowers

They call their credit limits “credit lines” to piggyback on bank terminology—knowing you’ll assume they mean true BANK lines of credit.

Know you want bank money—but give you credit cards disguised as “business financing.”

They hide the fact that their “business” cards report to your personal credit profile, tanking your utilization, risk, and future approval metrics.

They rely on the loophole that they can legally label credit cards as “lines of credit”—but ethically it is pure misrepresentation.

They never disclose that balances will sabotage your personal borrower profile and make bank approvals nearly impossible.

What They Count On You NOT Knowing

That true BANK credit lines always require a personal guarantee after the 2008 collapse—because banks now demand full-credit-risk accountability.

That credit cards reporting to your personal profile are approval killers, not business tools.

That some “business” cards are actually PERSONAL cards (Discover IT, Capital One Spark)—and these imposters poison your fundability.

That carrying balances damages your capacity for real credit lines because banks view them as high-risk behavior.

That personal “available credit” increases can actually LOWER future approval potential.

What You Actually Get

Misrepresented products disguised as “business financing”

Sky-high utilization penalties on your personal profile

Lower FICO® scores

Approval-readiness downgrades

No banking relationship leverage

A dead-end credit instrument with no graduation path

False sense of business credit progress

Day-to-Day FICO® Collaboration

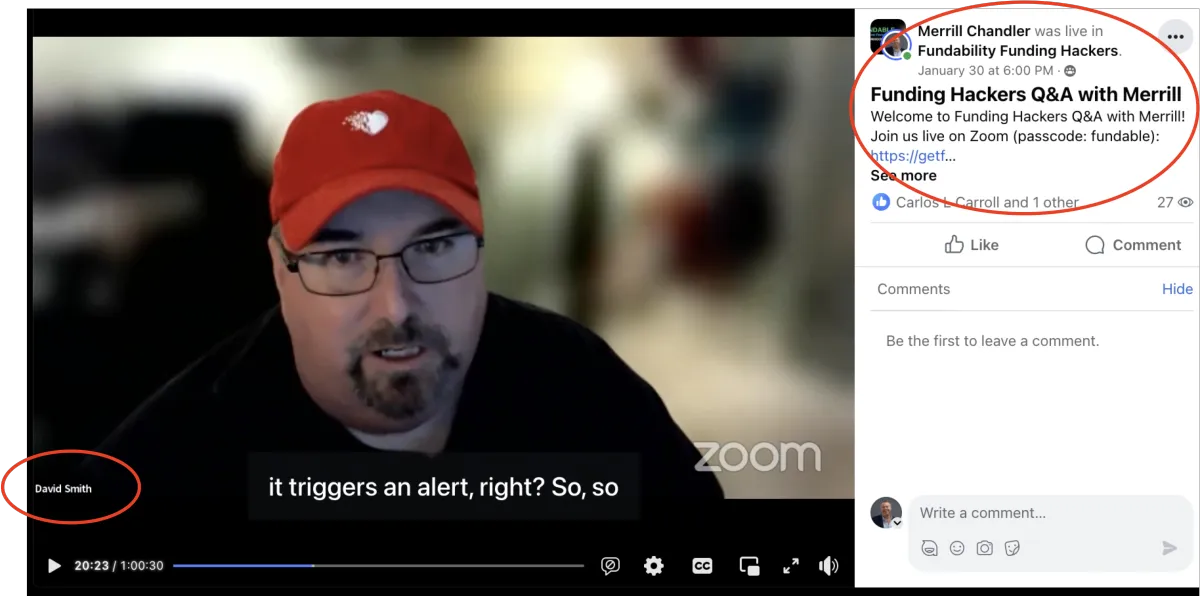

FICO® assigned us a dedicated liaison, David Smith, who has over 20 years experience as a leading expert in lending and originations. He’s the brains behind FICO’s Small Business Scoring System (SBSS), which banks use to approve business credit applications.

For over 8 years, David has provided us direct access to the data and tools that lenders use to assess borrowers so we can stay updated on the constant shifts in the financial landscape. In fact, he regularly joins our live Q&A sessions to answer YOUR questions about the lending and approval process.

Additionally, FICO’s Senior Director of Integrated Learning, Therese Henry, personally trained our team of advisors to better serve our clients. She helped ensure that every strategy we teach is aligned with FICO® standards.

This Get Fundable!/FICO® collaboration is unprecedented in the lending world and is a game-changing step towards Merrill's vision of creating profitable partnerships between borrowers and lenders!

What does all this mean for you...?

At Get Fundable!, we’re more than just advisors—we’re your partners in creating a credit and funding breakthrough. Merrill’s connection to FICO® ensures that every strategy we teach is grounded in what actually works.

Our mission is to help you go from stuck to unstoppable, turning "NO!" into "YES!" and unlocking doors you thought were closed forever.

Ready to Join the GetFundable! Movement?

We’ve helped countless entrepreneurs, real estate investors, business owners, and savvy consumers rewrite their financial stories. If you’re ready to take charge of your approval-readiness and finally achieve your funding goals, let’s make it happen. Together, we’ll flip the script and turn lenders into your biggest fans.

Our Funding Approvals Speak for Themselves...

This isn’t just guesswork. Every step of our Business Funding Approvals Path™ is rooted in the insider strategies

we gained from our 8-year+ collaboration with FICO® and years of successful implementation.

93%

1st Time Approvals

It's just math. The 5-Steps works for EVERYONE who applies the formulas. Do it and you too will get the approvals that you want to level-up your life!

$1,462,000

Founder Approvals

Merrill Chandler developed this process and optimized his own personal and business profiles for outstanding results...and it will work for you too!

$300 Million+

Our Community Approvals

Our community has been wildly successful in getting approved for the financing and funding that facilitated their business growth, and time and money freedom.

Check Out Our Free Resources...

Solutions Q&A w/Merrill Chandler

Every Tuesday at 3 pm (mountain) Merrill Chandler hosts a FREE Q&A session to help you avoid stepping on credit and funding landmines that will ruin your future approval opportunities. Come to a sessions BEFORE you:

• Complete ANY personal or business credit application

• Subscribe to a credit monitoring service

• Start an new company

• Engage credit repair services or do your own disputes

• Engage a debt consolidation "service"

• File for bankruptcy

• And any other credit, financing, and funding situation

Get Fundable! Podcast & Blog

With almost 200 episodes, the Get Fundable! Podcast does a deep dive on topics critical to your personal and business credit, financing, and funding success. Topic categories include:

• How your identity is the gatekeeper to your approvals

• How the 5 Fundability Factors impact your success

• What types of business entities are fundable

• Which businesses are classified as restricted industries

• How to identify business credit "imposters"

• How business codes make or break your success

• And many, many more

Frequently Asked Questions

Want to read instead of watch our Solutions Q&A or Podcast? Our Frequently Asked Questions is where our most important questions and answers go to hang out

Follow the link to scan for answers to your important questions.

Income and Result Disclaimer

While the results stated on this website are real results, they are not typical and in no way represent a claim by Get Fundable!, Inc. that you will receive identical results. Your results and the time it takes to achieve said results, will vary based on your fundability, financial situation, and speed of strategy implementation.

© 1997 - 2026 Get Fundable! Inc. All Rights Reserved.

Salt Lake City, Utah 84070

Privacy Policy • Terms and Conditions