Your credit cards impact your profile either for the good or the bad. In this episode, Merrill Chandler guides us in determining where ours stand by helping us understand what is called a revolving account portfolio. He also talks about what FICO is measuring and how lenders’ software evaluates the different credit cards – from personal credit lines and personal charge cards to credit cards. Join Merrill in this episode and find out how fundable you are and what a revolving account portfolio is all about.

—

Watch the episode here

Listen to the podcast here

Revolving Account Portfolio Quality

We’re going to take a look at your credit cards and their impact for good and ill on your profile, what FICO is measuring and how lender software evaluates these different credit cards. We call it a revolving account portfolio because you can have personal credit lines, personal charge cards, credit cards. We’re going to cover all that. I will tell you how fundable you are. Your credit card behavior, your revolving account portfolio directly impacts how fundable you are, the amount and the types of approvals that we’re looking for. Let’s go through the definitions of terms so that we are all on the same page. Are all revolving accounts created equal? They’re not. It’s not even close.

What message do your revolving accounts? There are two types of accounts on your profile. There are revolving accounts and there are installment loans. We’re going to define and we have sections for each one of them. They are going to blow your mind. What is the message that revolving accounts send the lenders? They say, “Look at all the money I have access to. Look at all this money and look how responsible I am with it.” There are two things that are in that message. One, if you only have $2,000 that you are responsible for, even if you’re responsible for it, it’s not as impressive if you have access to $20,000 or $30,000 or $50,000.

Three Types Of Revolving Accounts

Those limits also impact how much in your business is borrowing, the types of loans and limits you’re going to be awarded on the business side. Our whole game plan is when we say look at all the money, I have access to and I don’t run to Vegas, I don’t charge them all up and spend them all at once. I’m not risking the lender’s money. I’m super responsible. That’s what we’re looking for. That’s the message we want to send. We have access to money, but we don’t use it. It’s a massively important message. What is a revolving account anyway? Let’s cover this. The revolving account, there are three types.

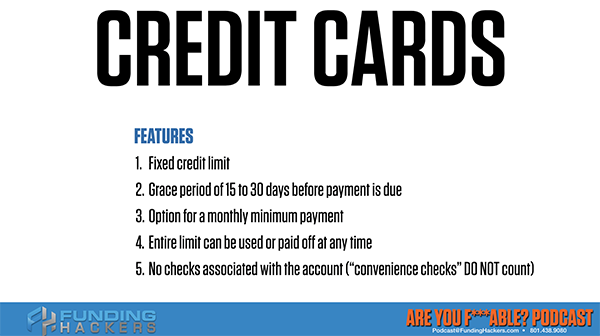

There are credit cards, there are charge cards and there are credit lines. Let’s go through and define each one of these terms. Credit cards have a fixed credit limit. There’s a grace period of 15 to 30 days before your payment is due. There’s the option for a monthly minimum payment and the entire limit can be used or paid off at any time. We’re going to learn that we don’t want to use the entire limit, but it’s available there. It makes you unfundable if you’re over certain a credit card threshold. Those are very important. There are no checks associated with the account and convenience checks don’t count.

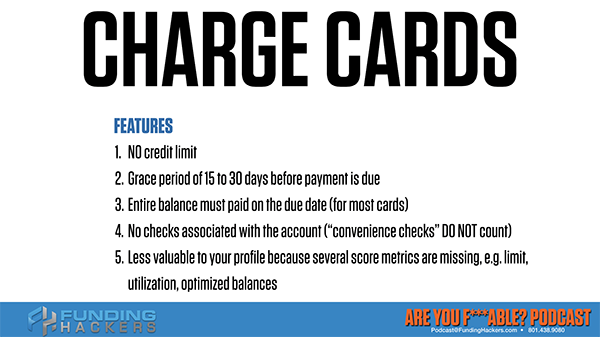

Convenience checks generally are like taking a cash advance. You might have a credit card that has convenience checks, but that’s more a cash advance and that does not count as literally like a credit line. A charge card is different. American Express’ Diners Clubs, different types of charge cards where there’s no credit limit. There is a grace period when the payment is due, but you have to charge off or you have to pay off the entire balance. As we’re going to learn, charge cards get a downgrade the value of that card’s contribution to your profile. Since there’s no limit, there’s no utilization. Utilization means the ratio of the balance to the limit.

If there’s no limit, they can’t calculate the same utilization models and it’s less valuable to your profile. You’re not closing any cards. Adult supervision is required. I’m going to tell you what’s valuable, not valuable, but you are not in any circumstance to close any cards that we even say are not ultimately valuable because we don’t know what they’re contributing to your personal profile. No closing. Adult supervision is required. I don’t know if I’m giving a revolver and putting it in the hands of a two-year-old. You must understand the rules of the game, but implementing it, getting through that minefield, you need a guide. I’m telling you to be very careful.

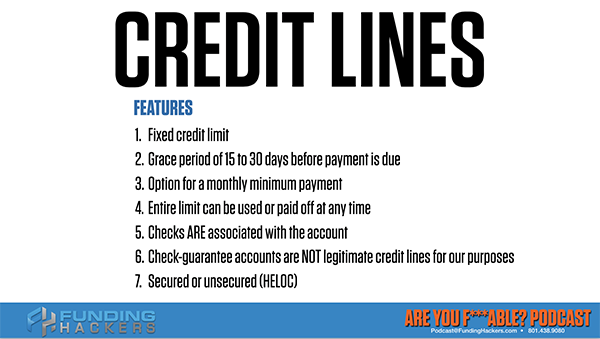

Here’s constructive and actual notice. I am not responsible for you blowing up your credit profile because you’re not understanding to what I’m telling you. By understanding, I’m not saying closing cards. I’m saying don’t close anything unless specifically instructed, which I may tell you. These are charge cards. No credit limits. It’s a 20% value deduction and you’re going to learn what that means. Credit lines are different. There’s a fixed limit. It’s like your credit card, fixed limit, grace period, minimum payment. You can use the limit or pay it off at any time, but there are checks associated with that account, but there’s no grace period. By and large for most credit lines, if you had your credit line long enough where you do have a grace period, count your lucky stars. The grace period, because the interest rates are lower, they start charging you the second you borrow it. Whereas a credit card is a personal loan for 30 days. Interest-free loan for a person for 30 days if you pay it off at the due date. Check guaranteed accounts are not legitimate credit lines for our purposes. They’re not.

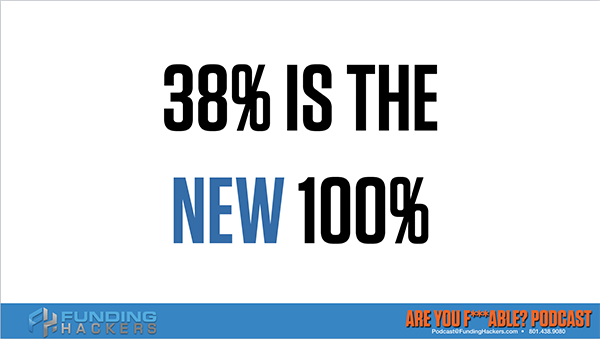

A check guarantee account, remember previously, when you use a check guaranteed account, that means there’s zero money in your checking account. You’re sending horrible underwriting messages to your current lender, “I got no money in my checking account.” We don’t want to send that message. Even though a check guarantee is a credit line, we don’t want to use it as part of our optimization and fundability™ process. You could have secured or unsecured credit lines like a Home Equity Line Of Credit, a HELOC, are backed by real estate. It’s still a line of credit. You can write a check and make something happen. All credit lines also come with plastic, with a credit card associated with it, but it’s like writing a check. The interest starts immediately. What is a good balance for a revolving account? 38% is the new 100%. 38% is the top. It’s the most you want to ever charge to a credit card without going into the risk department. When you charge more than the 38%, you end up in the yellow instead of the green zone for how much you’re using.

When you use a check guaranteed account, it means there's zero money in your checking account #GetFundable Share on XUltimately, you don’t want to be anywhere near 100% because you’re definitely in the risk department and they’re not going to raise those credit lines. They’re not going to raise the credit limits. Some people say, “Why 38%?” You may or may not know, but when your statement closes, let’s say you charge $10,000 on a $20,000 limit. $10,000 then they add the interest, 38% is designed to make sure you don’t go over 40% when they add interest at the end of the statement date. Do not carry a balance. I wanted to find two terms here. We call traffic, where you use the card and pay it off to zero. That’s traffic.

How much am I charging to the card? Utilization is how high my balance is when it’s reported. We have a whole section on reporting. If you’re carrying it over, that’s the utilization. Traffic is how much do I put on the card and then pay it off. Keep those terms clear because I’m going to use them and they are not interchangeable. Utilization is what we carry over, what gets reported to the credit bureaus. That’s what affects our utilization metric on FICO 40, but we don’t want to be over that 38%. Traffic is 10% to 20%. Utilization is no more than 38%. What types of revolving accounts are ideal?

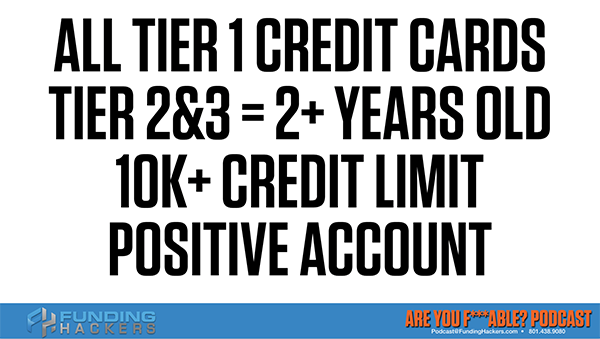

I’m giving you stuff that I’ve kept only on my high net worth clients. My full-service clients, I am telling it all. You don’t mind if I over-deliver. Is that okay with you? Ultimately after all is said and done, the only revolving accounts you want on your credit profile are what I call high-value credit cards, not credit lines, not charge cards. There are a couple of things I got to share with you. All tier-one credit cards, that is the first definition of a high-value account, and tier-two and three credit cards that are two-plus years old and $10,000 or higher in a credit limit and positive accounts. All tier-one credit cards that are not authorized user qualify as a high-value account.

Different Revolving Account Tiers

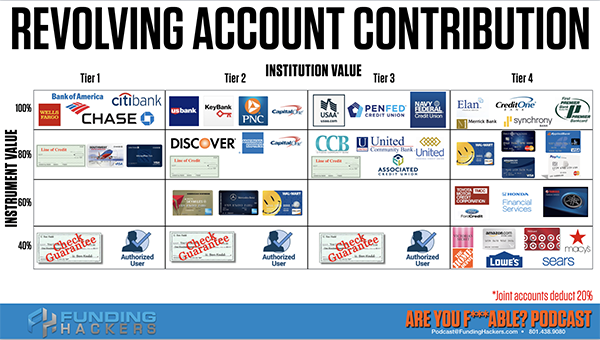

Tier-two and tier-three accounts that are two years old or more plus $10,000 or more, plus it’s a positive account. There’s no negative, there are no lates or anything else associated with it. That is what we call a high-value credit card. Ultimately, after we’re done with everything, that’s the only thing that’s going to help you have a professional borrower fundable profile. Remember that. Let’s take a look at all the different types of revolving accounts so that you can see how these things get graded. First of all, there’s institution value and there is instrument value, the value of the actual card contribution itself. Institutions go one through four, one being the best, four being the worst. Instrument value is 100% contribution to your profile versus all the way down to 40% contribution.

If you put that on a chart that makes it that there are sixteen different revolving account values by tier and by contribution. Let’s go through and describe what each one of these are. Tier-one is the national banks. When we were going over the FICO 40 characteristics, I talked about national bank cards. FICO counts whether or not you have them and what you do with them over the course of that 24-month lookback period. Limits traffic, its balances and utilization. Tier-one 100% is Wells, Bank of America, Citi, and Chase, the big four. That’s 100% contribution.

If you have a line of credit at Wells Fargo or Chase or Citibank, that’s downgraded 20%, so it’s an 80% contribution. If it’s co-branded, which means Chase is backstopping or carrying the paper for a Southwest Airlines credit card. That is also downgraded at 20% because now there are two parties responsible for carrying that paper. The joint accounts are also deducted 20% because there are two people responsible. One person being responsible for $10,000 is more powerful, higher impact than two people being responsible for that amount. Same thing on the reverse when it comes to the institution. If Southwest and Chase are both responsible, then there’s a 20% deduction in its value to your profile.

Remember that some of these are FICO, some of this is not FICO. Some of this is part of the algorithms that I have created and my team and what we do behind the scenes because we’re valuing how much of an impact it has on your business lending or all types of other credit approvals. This has been many years’ worth of experience and thousands and thousands of credit reports and thousands of clients. That’s tier-one. 40% is check guarantee credit lines. Check guarantee accounts are only worth 40% if it’s at Wells Fargo, Bank of America, Chase, etc. Authorized users, it may be a tier-one, but if you’re an authorized user on a Chase account, like in the case study a couple, you’re an authorized user on a tier one account, it’s a tier one institution, but it’s only worth 40% of the contribution.

That especially is straight out of FICO’s mouth. That is a tier-one and all the contributions. Tier-two, you got to remember all the banks are not represented. I’m going to define the types of banks so that you understand. Tier-two 100% cards are not just the ones that are listed. It is all regional banks that are depository institutions. The Discover and American Express and Capital One, the 80% group are marketing organizations. You can’t go to Discover and deposit money in their bank. Same with American Express and same with this division of Capital One. Notice that Capital One is both in the 100% range and it’s in the 80% range of tier-two. If you go to a depository institution and get a card there, that is tier-two 100% contribution because it’s a different value instrument.

If you go online or you respond to an email or a snail mail and you take advantage of the offer, don’t take advantage of offers. If you did and you’ve got this card, you just lost twenty points in its value contribution. If you look at the difference between those two cards on a credit profile, they have different names. They’re different entities, they are different financial institutions. Discover, American Express and Capital One is a 20% deduction. They are tier-two 80%. A line of credit, like a tier-one, at US Bank, KeyBank, PNC, the Depository Capital One, and all the other regional banks from them is downgraded 20% as well. This is important. That’s a line of credit. That’s not a check guarantee card. If you have a Discover or American Express that is co-branded, like American Express backstops the Delta SkyMiles card, that is deducted 20%.

In this example, the SkyMiles card is a tier-two 60% card and the Mercedes Benz is backed by American Express. That’s also a 60% value contribution. That the Discover backed Walmart Cash Card, not their merchandise card but their cash card. By cash I mean that you can use it same as cash or a regular credit card. The Walmart Discover backed card is also a tier-two 60%. You’re using insanely diminished values for all these. I don’t hold anything against you. If there are rocks to be thrown, we got to throw them at the institutions for not teaching us this. Some of this is part of my development and algorithms so that we can be more specific and motivate students, clients, borrowers to have the right high-value profiles.

Let’s continue to tier-four, same thing. Tier-two 40% cards, our check guarantee credit lines, check guarantee accounts. If you’re an authorized user on Discover, American Express, US Bank, KeyBank, etc., authorized users only get 40% of the points for institutions in that tier. The next one, we have tier-three. The tier-three 100% contributions are the national scope credit unions and savings and loans. You got USAA, you’ve got PenFed, Credit Union, Navy Federal Credit, the ones that have national scope. Those are tier-three 100% contributions. On the 80%, we deduct 20% value for all community banks and all local credit unions.

A credit union can have 100 branches over two states, but it’s still a tier-three 80%, because it doesn’t have a national scope. It doesn’t have national enrollment. The line of credit is from USAA or PenFed or Navy Federal, etc. These are all personal lines of credit. These are not business lines credits. There’s a 20% deduction for having a line of credit because that instrument can be abused far more easily. That’s part of the reason why we have a credit line deduction of 20% because it can be abused more easily. It’s so much easier to use that in times of trouble, times of financial stress, financial injury, etc. Finally, like all the tier-one and tier-two, tier-three, any check guarantee card and any authorized user rates at 40% of the possible contribution points to your profile. Here’s where it gets ugly. Let’s look at tier-four now. Credit One Bank, Elan Financial, Merrick Bank, Synchrony Bank, First Premier Bank. Bless their hearts, I call them predatory lenders because when you get on a bankruptcy list, a judgment list, a lien, it shows up on the public record. These are the guys who send you notices to borrow their money.

If we're going to become professional borrowers, if we're going to be able to leverage our personal profile for a business or large borrowing projects that we're doing, we have to be professional borrowers in the eyes of the lender #GetFundable Share on XThere’s only one circumstance in 1,000 where I would recommend to a student or a client to even consider one of these and it’s too deep of a dive here. We do not want to use these cards and if you have them, tier-four is where you start getting negative indicators on your credit profile that say a consumer finance account is showing on your profile. It’s a negative indicator by FICO that you have resorted to subprime money. Subprime money, whether it’s a mortgage, whether it’s an auto loan or whether or it’s a revolving account count against you every single time. These are a 100% contribution on tier-four because some of them are depository institutions.

How To Detect A Finance Company

They are financial institutions. The 80% where we lose 20% is where we have this first progress. The Amazon Rewards where you only get to by Amazon merchandise. There is Applied Bank, there are PayPal Extras. All of those online. Some of them same as cash, but they’re finance company. I’m going to show you how to detect a finance company, a card, but these are downgrade 80%. Notice over here, Toyota Motor Credit, the Honda Financial Services, Yamaha Financial Services, they’re in tier-four, but they’re down at 60%. We think those are legit, but these are revolving accounts.

When you go to buy a WaveRunner or an ATV, a motorcycle and you need financing, they will try and put you in one of these types of instruments. These are not good. They’re financial services rather than a depository institution, and in the worst possible way, these are tier-four accounts. They show up as a negative indicator because there are derogatory indicators on FICO. There are negative indicators. It’s a negative indicator that says that you are resorting to a finance company. There is prejudice against your profile for finance companies because more people who have finance companies on their account default more often and go bankrupt more often. It’s part of their math and I trust their math, and more importantly, the lenders trust their math.

Also, the bad thing about these is that if you pay off your ATV, you still have an open account, so you’ll buy another one or buy a WaveRunner or put finance more. These revolving accounts are no bueno because they’re designed to be used. Remember #NurtureYourGoldenGoose, #FeedYourGoldenGoose? They’re using these to carry your paper, to carry your WaveRunners, ATVs and recreational equipment, that’s not what your personal profile is designed to do. Your business profile where it doesn’t report to the personal, where it doesn’t harm your personal. We do all of our work over on the business side of things, all the heavy lifting and carrying of debt or otherwise.

The personal side is that golden goose that we nurture, we take care of and all those golden eggs turn into awesome opportunities for funding for us. The last one, don’t hate me here. All the junk store cards. Remember the cards that we talked about that were on the case studies? Robert and Chris’s case studies. These are the worst possible indicators, the worst possible credit you can have on your personal profile. These scream Victoria’s Secret, Amazon, Target, Macy’s, Sears, Lowe’s, Home Depot. If you’re a real estate investor, you put Home Depot on your business, not on your personal. We don’t know this, they didn’t teach us this. We should be angry at the system and furious that we didn’t know. Let’s now learn and start implementing this stuff. Don’t close any accounts. Tier-four 40% are junk cards. They are the worst possible cards because you’re buying merchandise. They’re not cash cards and FICO gives you poor marks. They reduced the value and fundability™ of your profile because you have these cards on them. They give you a negative indicator in the process.

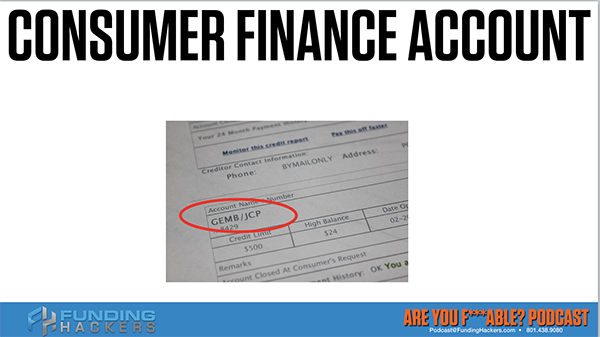

I’ll show you how to detect them. The ones I’ve named, the ones I’ve shown you, they are not a complete list. I’m giving you the types. National banks, regional banks, national scope credit unions and local scope credit unions and community banks. These are all here, but this is not the complete list. There are literally hundreds of junk cards. Every single mall has a merchandise credit card and you’re going to learn that they have some pretty interesting ways to ruin your profile without you even knowing it. The moral of the story, mall store cards equal consumer finance accounts, which is the actual word language to look for on your myFICO report and junk card.

One of the things we are going to is I’m literally going to go through and interpret a myFICO credit report for you. Start to finish, we’re going to go through the entire FICO credit report. That’s going to be amazing. I can blank out all the names and account information, but I want to show you how to read, what to notice, what FICO is not telling you on that report and we’re also going to do one on how to interpret your consumer disclosure files, Equifax, TransUnion and Experian. Every one of these, I want you to know how to look at your 24-month lookback period. We’re going through all of that.

Remember that shot sheet that I shared? We have hundreds of things to talk about so keep reading. I want you to be making powerful financial decisions for the rest of your life. Consumer finance accounts equal junk cards. How do you know on your credit profile what is what? It’s simple. The General Electric Money Bank, GEMB. General Electric Money Bank/JCP, JCPenney. If there is a slash, then that means General Electric Money Bank is carrying the paper, is financing the purchases for JCPenney. That’s how you know that it is a consumer finance account.

That’s how you know that you’re getting a negative indicator by FICO on your fundability™ and you got to know that those 40% junk cards dragged down your fundability and prove you are a consumer. It’s literally screaming to lenders, “I am a consumer. I am not a professional borrower.” Are you with me? Do you see how this works? If we’re going to become professional borrowers, if we’re going to be able to leverage our personal profile for business or large borrowing projects that we’re doing, we have to be professional borrowers in the eyes of the lender. We’ve got our paper, our credit profile. Our data have to look spectacular.

This next section is I’m going to show you how to ruin your credit and save 10% on your next purchase. How many of you have done that? How many of you have taken that pitch where it’s Christmas time or you’re back to school and they’re like, “If you fill out this application, you could save 10% or 15% on your next purchase.” You have to spend $30,000, $60,000 at Target or Kohl’s or whatever to even make it worth it, worth the damage to your credit profile. First of all, there’s the inquiry, depending on where you are on the credit score pyramid. Remember how we talked about the credit score?

Wherever you are on that pyramid, you’re going to get a three to fifteen-point loss on that period. That inquiry is going to because of three to fifteen-point loss. Also, if you’re approved, you’re going to get a 40% low-value junk card. You’re getting a new junk card and that junk card will lower your average age on everything. The value of your revolving accounts portfolio diminishes, decreases significantly. I’m going to leave you hanging here because we’re going to get into how the average age and the age of your accounts contribute to your profile or how you’re butchering your golden goose.