There are so many credit-related scams these days, and more and more people are getting away with it. Today, Merrill Chandler gets to the bottom of these business credit-building scams. Using Dun & Bradstreet CreditBuilder Plus as an example, Merrill helps us understand the difference between business and personal credit reporting. He also shows how these scams work or how scammers lure you into their credit traps. Don’t miss this episode to learn more about how to avoid these scams.

—

Watch the episode here

Listen to the podcast here

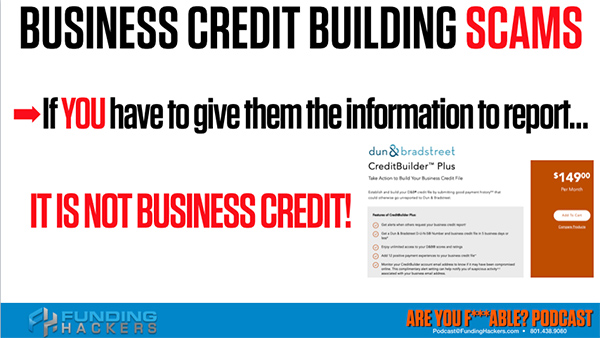

“Business” Credit-Building Scams

We’re talking about how literally business credit and the perpetrators of these fake notions of what business credit is where they literally try and make us climb the wrong tree. That’s why we’re calling this episode the Climbing the Wrong Tree Building Business Credit that is Actually Meaningless to Lenders. Let’s get to the bottom of what we’re actually talking about. Now, business credit building scams have one principal to it that covers everything and all the business credit builders out there. If you have to give them information to report, it is not true business credit. If you have to give them information, meaning you give it to them and then they report it, it’s not business credit. Because it is your information and you’re curating it, you’re choosing it. You don’t give your credit to Experian, Transunion, and Equifax. They are collecting it from the third-party reporters: the creditors, the lenders, the cell phone bills and the collection agencies. They’re collecting it and then they make a credit report and build a profile based on that information. That’s our first hint that this is the scam of scams. If you have to give them the information to report, then it is not business credit.

CreditBuilder Plus

I used an example here of the Dun & Bradstreet CreditBuilder Plus. Let’s take a deeper dive into that business, CreditBuilder Plus. First of all, they want to charge you $149. I said this once before, I’m going to say it again over and over that business credit reporting does not follow the same rules that personal credit reporting does. They don’t have to. There is no Fair Credit Reporting Act for business credit reporting. If you look at the business credit reporting environment, you’re going to see the people who score the data, FICO and even the subsidiaries of the credit bureaus and VantageScore, they’re all different companies. You cannot report the data and score your own data. A third party has to do it. That’s one of the things that we want to look here is that Dun & Bradstreet is literally telling us, “We will build your credit for you.”

Let’s look at one of the features that they offer here that feature for $149 a month, they will add twelve positive payment experiences to your business credit file. We’ve gone through these deep dives numerous times. examining, credit reporting, unweighted scores versus weighted scores and FICO versus FAKO scores. You pay them $149, and then you go collect twelve vendors and you give that payment information to Dun & Bradstreet and they will call those individuals and verify that those payments are on time. You’re ratting yourself out. You’re providing the data. For $149 a month, you get to build this credit profile with Dun & Bradstreet. The thing is, as I’m going to show you in every one of these, the lenders, the business credit line lenders, the business loan lenders, even the business credit cards do not look up your Dun & Bradstreet, your D&B rating. They don’t look up your Experian business.

They rarely look up the Equifax Business Credit Reports because those credit reports have information. Remember a few episodes ago where we said that they hold the information, they report the information, but they’re not being accountable with how they’re using that information. Let me give you another example. eCredable has come online saying, “Dun & Bradstreet has the corner on this market. We want to get into business credit building scam like everybody else.” What do they do? They make an offering. They say, “eCredable makes building business credit as easy as paying your bills.” Why? You do the exact same thing that you do with Dun & Bradstreet. You provide your power, your water, your gas, your mobile phone, cable, satellite, TV, internet and landline. You give them the information and eCredable we’ll create a business profile that is eCredable profile.

If they add it to Dun & Bradstreet or if they added Experian Business, do you think for a second that Chase, Wells Fargo, Citi, BB&T, any Tier 1 or Tier 2 bank who offer the very best business loans and business credit lines at the very lowest rates, the very things that those trophy lines that we’re looking for. Do you think they’re going to give you a $50,000 business line of credit on your water bill reputation or on your cable TV reputation? It’s not going to happen. It never has and it never will. The reason why I call them scams is because since you don’t know the difference you’re thinking, “I want my credit reputation. I want a business credit report. I want business credit because I’m looking to get credit lines and loans for my business.”

Business Credit Reports

There is a vast chasm guy. There is a huge gap at why does the Grand Canyon in financial terms between these types of business credit building scams and business lending metrics that are being used by the big lenders. Now, one of the biggest ones out there is Credit Suite. Their advertisement is, how to build credit for your EIN that’s not linked to your SSN? That’s an employee identification number. Link it to your business and not to your personal and that sounds great. They’re like, “Let’s do that.” Here’s what’s fascinating. Here are the five steps straight from their website where get business credit reports. Whatever business you’re operating under, they say get the business credit report. That’s Dun & Bradstreet, Experian business and Equifax business. No harm, no foul. I tell you to do the same thing.

We have to know the rules of this game so that we can create it #GetFundable Share on XThe next thing they do is they say, “Let’s apply for vendor credit.” Vendor credit is broad based. It could be for fixing flippers out there, for you retailers, it could be a paper supplier. It could be a carpet supplier or your cabinetry people. It could be Uline. Credit Suite pushes Uline. Now remember, traffic is still a thing. For anything to matter, you can’t own an account. You’ve got to put traffic on it. By the way, these five steps take eighteen months to accomplish, but when you get to the eighteen months, I’m going to tell you exactly where you end up. Applying for a vendor credit means to get those trade lines or if somebody supplying something to you. There’s Retail Credit. That’s your Home Depot for the business. It’s true, if you know what you’re doing, you put it on your EIN. You don’t put it on your personal profile. You put it on your business profile. With retail credit, you can do Federal Express. It’s a great retail credit. Sometimes that can be under vendor credit because they’re hybrid between the two. Retail credit is Staples or Home Depot or Lowe’s or any retail credit that services the business community. That’s step number three, apply for retail credit.

You pay that for a few months and you’re running traffic. These are three to five what they call trade lines. Step four is to apply for fleet credit. That means to get a gas card, but get two to three of them, minimum. Now, we’re sitting here with gas cards and it’s still all merchandising. Up to here, steps two, three and four, vendor credit, retail credit and fleet credit, it’s all 100% merchandise. Even the gas, you’re buying a commodity if you’re not getting cash credit. They wait until step five to go to cash credit. Cash credit means you’re getting a cash credit card but here’s what’s interesting. These cash credit cards are few and far between what we have called in the past their tester limits. They want you to prove up.

After eighteen months, you’re applying for cash credit but many of these cash credit cards report to your personal. It could be the Spark, because they’re saying you’re applying under your EIN, but they do not take into account truly the personal credit reporting versus the business credit reporting. The cash credit is low limits. Nowhere in here guys, is there consideration for getting a business loan or using these credit markers, these credit accounts, this reputation to build so that you’re going to acquire the trophy credit lines that we’ve talked about in this entire show.

Let me tell you about Brad, my partner in the business. Brad actually has a meeting with one of these guys because we’re trying to suss out back in the day. A few years ago, we’re looking what is business credit, how does it work and etc. He has a conversation with one of the VPs at Credit Suite and he literally asked the question, “If I go through your entire eighteen-month program, can I get a bona fide business line of credit for $20,000, $30,000 or $50,000?” Without hesitation, the VP answered, “No, that isn’t what this is for.” The intelligence of the question begets the intelligence of the answer. Until now, we haven’t known what business credit really is. We pay these guys gobs and gobs of money to build our credit with Dun & Bradstreet, to build our credit with eCredable and to build our credit with Credit Suite. This is not okay.

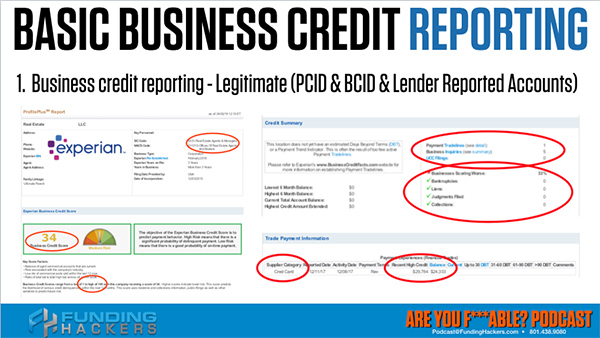

Business credit reporting does not follow the same rules that personal credit reporting does #GetFundable Share on XThe other thing that what legitimate business credit reporting are Dun & Bradstreet does collect data. The data is very sparse, it’s very elemental and it’s very basic. Equifax has a business credit reporting process and so does Experian. The thing is, each one of these collect data, but it is substandard. It is not even 10% of the accuracy and thoroughness that personal credit reporting is. Remember I told you the Dave Smith, the Small Business Association liaison between FICO and the government told me straight up that business credit reporting is what personal credit reporting was literally in the mid-1980s. What are we going to do? We have to know the rules of this game so that we can create it. Let me bring up one of my client’s credit profiles. I took out the name of everything but I want to show you what this actually means.

Business Credit Reports Landmines

This data is used by FICO who as we said is entering the business credit reporting space and is going to take over the business credit reporting space and it’s going to be amazing. I trust FICO, lenders trust FICO. As soon as FICO starts gathering all this data, it’s going to be so much easier to move and even get approved and use automatic underwriting in the business credit space. Right now, it’s the Wild Wild West. We have amazing work around to navigate these waters. There are credit lines for the taking if we meet the underwriting guidelines. Let me show you a couple of things that are huge landmines that we need to watch out for on these business credit reports. I’m using Experian as an example. All three business credit reports have some of the same problems. Notice the name of this company was real estate something LLC. Real estate LLC is a red flag word because that’s one of the things that are not fundable when it comes to SIC codes. The SIC code and the NAICS code is real estate agents and managers, offices of real estate agents and brokers. The two designations are red flags. This is going to create a denial.

When I showed you the approval process where FICO takes the personal profile and then goes and checks the legitimacy of the funding entity, the QFT, the Qualified Funding Entity. When it checks that entity, it’s going to get a big fat no here because real estate is not fundable. It is what they call a high risk. In our world, it’s an unfundable SIC code. You’re going to get thrown out with the bathwater. It says payment trade lines. There’s one. The details are down here but notice it says under trade lines it says, supplier category. It’s a credit card. It doesn’t say what lender, it doesn’t say the limit or it says that the date reported was 12-11. The activity date was 12-8 of 2017. Payment terms were revolving which is fine. The recent high credit was 29. That means kind of the high watermark that we’ve talked about in our previous episodes on Balances and Utilization, but over here it just says the balance, 24. There is no zero. There is no reporting of the utilization, the due date. There’s no 24-month look-back period here. There is nothing that gives us any data about the type of account. Five business inquiries, UCC filing, zero and business scoring, they said, “There’s no collections, judgments, liens and bankruptcies.” Notice even that is looking into your personal profile.

The trade line information says credit card with no real and a recent balance. None of that is actionable intel guys and we got to understand this. The next thing is the business credit score is 34 out of 100. 100 is the range for Experian’s credit. No bona fide business credit lines, business loans and business credit cards are using these scores because they don’t calculate anything. There’s no utilization. We don’t know if the limit is $25,000 and that would make this a $24,000 like 98% utilization or we don’t know that it’s $100,000 and it’s only 25% utilization. We have no actionable intel to evaluate this account. No algorithms can evaluate this account. That’s why FICO was coming in here and it’s seeing the wide-open country.

The biggest credit scam that we can talk about is the travesty that once again businesses are taking advantage of borrowers because you don’t know the rules of this game. I wanted to show you this particular report because this gentleman comes to me and he is a baller. He is a businessman. He’s amazing, extremely successful and has literally a ten-figure income. Originally, he was in real estate. When he went through this process and got to evaluate, it was like I had pulled his fingernails out because he could not believe that real businesses were so not legitimate. This business credit reporting, legitimate PCID and a business credit identity accounts. It was interesting to watch somebody who is new to fundability™ and new to getting fundable. Finding somebody saying, “How can they do this? How is it possible that there is such bad record-keeping? All this business credit that’s going on out there, how is it that there are so many scams? How is it that people are getting away with this?”

That’s why I started this show. That’s why I do what I do with my bootcamps. Go to GetFundable.com and check out the bootcamps if you want to make all of this actionable in a single weekend. I’m doing this because it is not right at all and I’m tired of it. How do you grade this as a 34 when there’s no information here? There is no bad information at all. How do you grade something when there’s no information? We’ll pick this up on our next episode. I’ve got a few more things on business, then we’re going to get some great stuff on your installment loans. I’ve got some episodes that are going to be on the road. At least according to me, nothing but amazing stuff is coming at you. I want you to keep bingeing, take this seriously and if you’re not already f*able, get as f*able as you possibly can be, as fast as you can be.