Banks and smaller businesses rely on FICO to measure our credit line with their algorithms. That is why it is important that we have some knowledge with regards to how we are being measured as it would give us an edge to have a better credit score and make us more fundable. Host Merrill Chandler the FICO algorithm and what they really measure, revealing the 150 borrower behaviors that can affect your fundability™.

—

Watch the episode here

Listen to the podcast here

Uncovering What FICO Really Measures

The 150 Borrower Behaviors You Never Knew Mattered

We’re going to be talking about one of the key meetings that we had in FICO World 2019. I had the opportunity to schedule an appointment with Ethan Dornhelm. He is the contact that we’ve spoken with back in the FICO World 2016. We got to spend tons of a great time with him and his FICO score development team asking that 100 questions that I’ve referred to. In the revisit, we scheduled another meeting with Ethan and to our surprise and amazement, he invited Tom Quinn, the VP of Scores to join that meeting in his stead. Tom is the Manager over the development of MyFICO.com, one of the things that we live and breathe by. The first iteration of MyFICO.com in the early 2000s came from Tom Quinn. We had a chance to meet with him. One of my biggest questions was about what we call the FICO 150. They don’t call it FICO 150. I’m trying to make it intelligible to all of us borrowers. These Reason Codes are the total collection of all the of the things that keep you from fundability™.

In the FICO score algorithm, we learned that there are twelve scorecards. There are four scorecards for negative credit and there are eight scorecards for positive credit. This was an update from what we’ve shared in previous episodes. These scorecards parse out the FICO 40 characters that are being measured by the bureaus. The bureaus have the data, FICO, and each one of the credit bureaus separate databases has an onboard scoring system. Their software is on the mainframe at the credit bureau. When you do an inquiry, it goes to the credit bureau and the data that is coming back to the merchant, whether it’s an auto loan, mortgage or credit card, passes through the FICO’s software. Each bureau has subtle differences in how they collect the data. FICO has specific mechanisms for measuring that data.

That’s why in the previous episode where we talked about FICO 542 which is the version of the scoring software from the ‘90s. It represents Equifax, TransUnion and Experian as different indicators, FICO 5, FICO 4 and FICO 2. Here, all of these FICO codes, as Tom Quinn shared with us, some of them are from previous like the FICO 542 or FICO 8. Some of them are FICO 9. Some of them are future and forward casting that will be included in either future versions of FICO scoring software or there already being measured in the relationship with FICO in helping lenders develop their underwriting software.

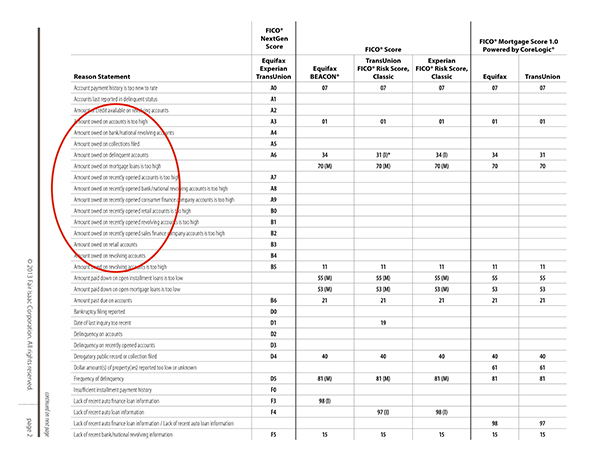

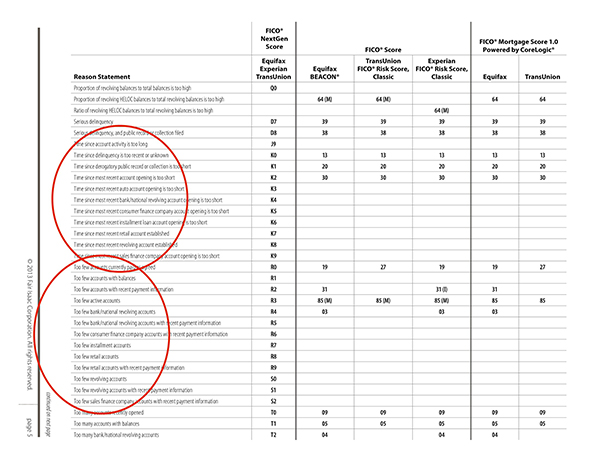

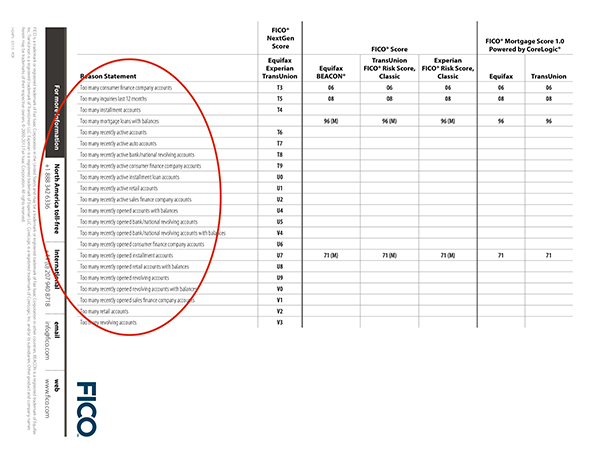

Some of the big ones were also told at the meeting, the Chases, the top tier banks, many of them have their own scoring models where they don’t need FICO’s support in creating those internal performance measuring algorithms. The tier twos, tier threes, all of those regional banks, the local community credit unions and community banks who are subscribed to FICO, every one of them have FICO supports in shaping their algorithms to coordinate with FICO’s evaluation of your profile. What we’re going to be going through is a broad base. There’s no way that we can go through every single one of these, but I want to show you the big things that they’re looking for. These codes are over the 24 months lookback period in increments of 3, 6, 12 and 24 months. There are eight major categories that we’re going to be reviewing.

Less is better than more when it comes to balances on your credit cards #GetFundable Share on XFirst and foremost, let’s look at Experian, TransUnion and Equifax. Here are the indicator and the old version of the name, Beacon, Classic and Experian Risk Score Classic. These are what was called 542. There are mortgage scores powered by CoreLogic. They’re showing every one of these and where they fit, which are being included in the current models. I want you to understand that what we’re looking at here is that they’re giving us what valuations are being measured in the next-gen score, which is FICO 8. FICO 542 is Beacon and the two classics. These indicators show, which one is being used in which version. For example, look at the difference between 542 and what they’re measuring. There are two spaces and these mean that those are being used in the next-gen, which is the FICO 8, but they are not being used in 542. Now that we know the playing field, let me tell you what they’re measuring.

We can’t go into all of these, but I want you to see what’s out there. First of all, the amount owed. All of those criteria have an amount owed. There is amount owed on collections, on a delinquent account and on recently opened consumer finance versus the amount owed on recently opened bank national cards. It’s too high. Notice that they’re saying recently opened versus just amount owed on revolving accounts. They’re distinguishing between recently opened retail accounts, recently opened consumer finance accounts and open bank card and national bank card accounts. They’re evaluating these separately. We know that sales finance companies are too high. The sales finance companies could be furniture, auto loans from finance companies or tier four. That can be in there. Open revolving accounts are too high and retail accounts. That’s your tier four 40%, what we call the junk cards.

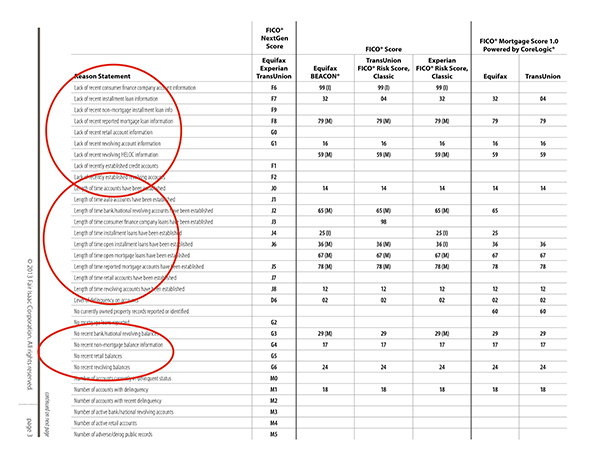

That’s different from the consumer finance company account, which is like some of the fintechs, the SoFis, the Prospers or the Marcuses from Goldman Sachs. Do you see how we have broken down into tiers the different types of accounts? In FICO 8, they’re evaluating those separately, whereas they did not evaluate those in earlier versions of the model. They still have, amount paid down on mortgages is too low, amount past due on the account and bankruptcy filing. There are numerous versions, but let’s go to the next page. Notice that it’s lack of a recent consumer finance company account. If you have a consumer finance company, but it’s not reporting faithfully, you may get triggered on the lack of recent data.

We talked about accuracy being the key to success and repetitive. If it’s open, you’ve got to put traffic on it. Unless the objective is that you are working with us and our objective is to close it, then there are strategies on how to close that once we’ve replaced the low-value points with high-value points. Lack of recent non-mortgage installment info, revolving account, revolving HELOC and established credit accounts. There’s a whole slew of it. There’s another large category that’s being measured. There’s the length of time accounts has been established, length of time that they open installment and open mortgages. Length of time retail accounts have been established and length of time revolving accounts have been established.

You can't have too much available credit #GetFundable Share on XEvery one of these, there’s not just lack of recent, but the length of time that these things have been established, your accounts have been opened. As we’ve said, 3, 6, 12 and 24 months, an account doesn’t even register as valuable until it’s at least 24 months old. If you’ve got these lower retail accounts in your way or they don’t even count the 40% of the value of a high-value account, you’re not getting any juice because even the length of time counts against you. That’s why we say in the Bootcamp, if you opened up a retail card in the last few months, I recommend to people to close it and take the score hit, it will rebuild over the next 3 to 6 months. After a few months, in that 6 to 12-month category, that length of time is counting towards it. We don’t want to mess around with that.

The next one is no recent national bank revolving balances. In the 2016 FICO World, Ethan told us that less is better than more when it comes to balancing on your credit cards, but some are better than none. If there are no recent bank card revolving balances that they are reporting, you’re not getting the juice from G2 as it contributes to your fundability™, no recent non-mortgage balance. They’re saying balances on mortgages, but there are your other installment loans, auto loans and student loans. If you don’t have any auto loans, student loans or otherwise, you’re not getting the point contribution to your fundability™ and not just your score, no recent revolving balances and no recent retail balances. If you got a card and if it’s registering that you have a low-value card, but there are no balances on it, that means there’s no traffic. That means you’re not giving the algorithm something, “What have you done for me lately?” That’s why we need to close them or do something with them to maximize our fundability™.

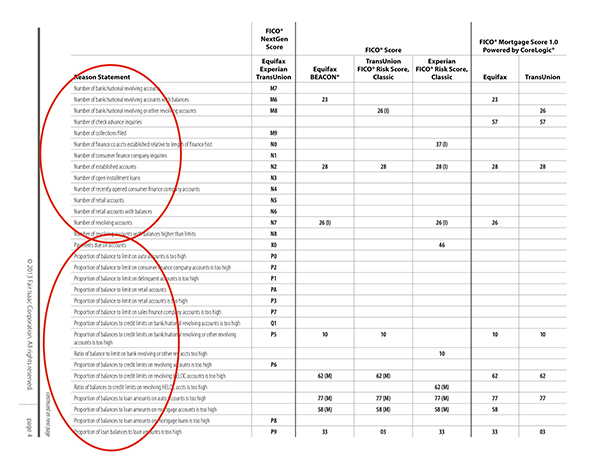

We go to the number of banks and national revolving accounts, the number of checks advance inquiries, and the number of collections filed. How many of these different things? You can’t have too much available credit. They are counting the numbers towards each one of these. This is vital to what we’re learning. Again, the proportion of balance to limit on auto loans, consumer finance company accounts, on delinquent accounts, proportion of balance to limit on even accounts that are delinquent, proportion of balance to limit on sales finance. They’re breaking all of these out.

That’s why we give them tiers and value contributions and then the ratio and proportion of balance. There’s a ratio of balance and proportional balances to limits on even your auto loans, student loans and consumer finance cards. They’re calculating your balance to limit ratios. Finally, we go to time since the derogatory public record is too short. Time since account opening, time since most recent, time since, that’s another way of evaluating. There are patterns here. We have the global patterns and we have the smaller that I’ve outlined. These smaller groups that I’m reviewing with you are the smaller valuations that they’re giving these different accounts.

We have too few national bank cards, too few installment loans and too few revolving accounts. For the retail accounts, if those are the only accounts you have on your profile, you can have too few. We’ve talked about in previous episodes about what the balance or what the perfect profile looks like. If you don’t have any other bank cards or national accounts, you need to have the right number of consumer finance accounts or trade lines. We don’t want you to build those, but I’m telling you how they score it. It needs enough data to establish some pattern of behavior for you, hence, fundability™. Finally, you’re going to have too many installment accounts, too many active autos, too many of lots of things and too many recently opened. Go back to the episode on 524 where you can’t open too many revolving accounts too fast. Too many things, too many recently opened retail accounts, too many open revolving accounts, every one of these is going to go up against you.

I can’t go into all the details of every one of these, but these are the behaviors that are driving your fundability™, too many, too few, not enough, all of them. We’ve already offered the opportunity to be able to get the PDF of all the Reason Codes. This is what it’s about, getting into the details and finding out what behaviors they’re measuring. I’ve given you an example and the resources to discover it. The only thing is every single one of those behaviors has a custom application to you. If you would like to know more about that, go to GetFundable.com and click on the Bootcamp. Join us and fill out the fundability™ documentation. We will make sure that you have more answers to your personal questions than just reviewing the high-level view. My intention every single time that I do these shows is to make sure you are F*able.

Important Links:

- MyFICO.com

- CoreLogic

- Bootcamp tab – Get Fundable

Bernardgon

September 21, 2020 4:56 pmThank you very much for the information provided

I’m very impressed

Terrysag

September 21, 2020 4:56 pmVery interesting to read you

Good luck to you