An aim towards positive account scoring with the maximum number of points possible for your file is a necessary goal. Merrill Chandler shows how this can be achieved by sharing the actual secret list that FICO uses to evaluate your fundability and how it corresponds with the lender underwriting software. Merrill emphasizes on the essence of optimization – increasing fundability points and decreasing negative drag against your profile. He also points out the importance of understanding what is being measured.

—

Watch the episode here

Listen to the podcast here

FICO 40 And Optimization

We have got a crazy, awesome episode for you. First of all, we’re going to be discussing the actual secret list that FICO uses to evaluate your fundability™ and how it corresponds with the lender underwriting software. We are talked about FICO. We talked about the underwriting software. I’ve even talked about the origin story where we talked about meeting with FICO and the individuals who were the liaisons between lenders, software developers and FICO scoring developers. There’s an entire collaboration to make sure that the FICO 40 measurements are being implemented and used in the software for the lenders.

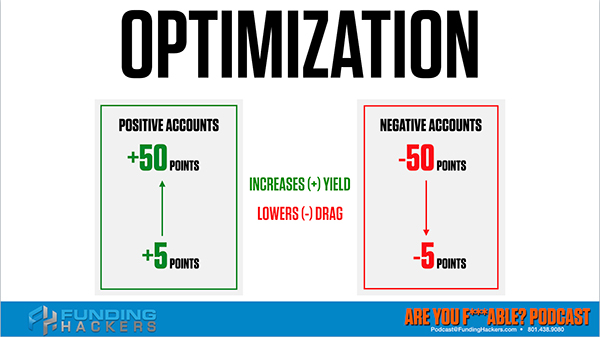

FICO List On Fundability™: The essence of optimization is to increase the positive fundability™ points and decrease the negative drag against your profile.

In this episode, we’re going to discuss that insider list of what FICO uses. We don’t have the time or the resources to go through every single one on the list, but I’m going to share with you the list and send you out to go find it for yourself. The issue is this is not whether or not the list is available, it’s what to do about it. These are triggers. We’re going to be talking about those triggers. How do you optimize a borrower profile? How do you even know what it means to optimize a borrower profile? The first thing you have to understand and we’ve talked about it, is learning what is being measured.

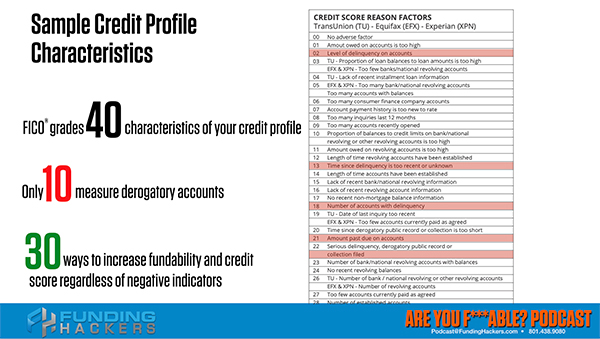

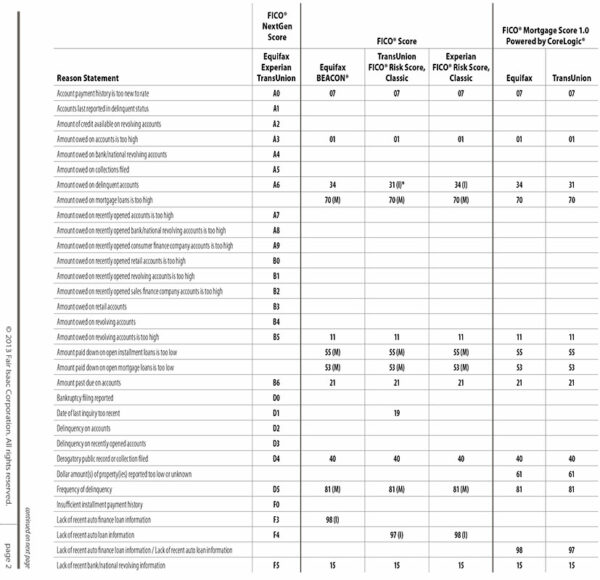

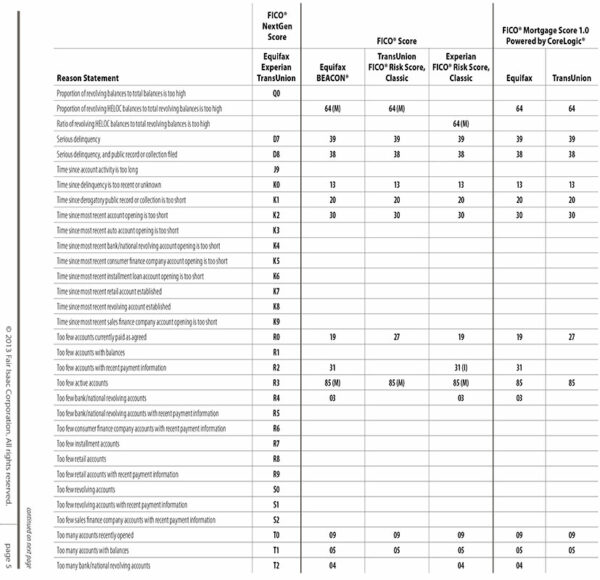

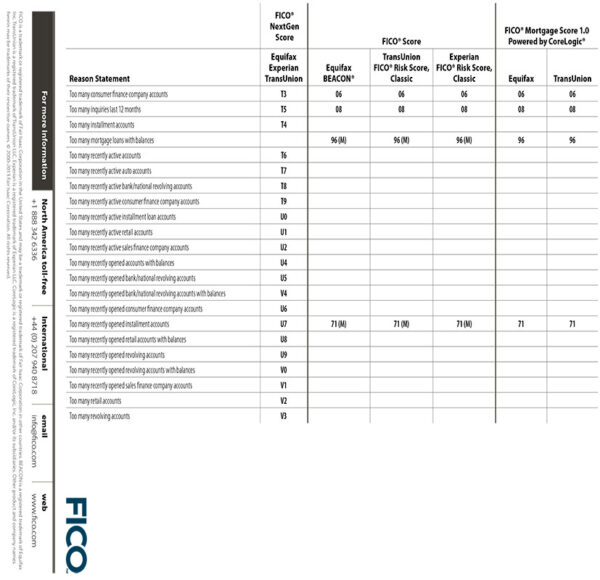

If you don’t know what’s being measured, you’re going to be distracted by those shiny objects we call credit scores. We’re past that. Those are rookie moves. We need to make sure that you understand what is being measured. Let’s take a look at the 1,000-foot view of this. FICO measures 40 characteristics of the credit profile. Ten of those measure derogatory accounts. That means there are 30 ways to improve your fundability™ and raise your credit score without even addressing any of the negative accounts. What are in red are the derogatory account indicators or at least some of them because the list goes on.

If you want to find this, you can Google credit bureau reason codes. Look up reason codes. There is a grip of them and you’ll understand why FICO 542 had special algorithms for Experian, separate ones for TransUnion and separate ones for Equifax. What I want to point out is that we have clients who have 800-plus fundable credit profiles with derogatory accounts still on their profile because you can optimize the other 30 characteristics that we’re talking about. Let me review some of these so you can understand why I’m giving you everything that’s possible.

There are instructions or there are insider secrets to every single one of these but notice too many inquiries in the last several months. There are too many accounts opened. Remember, there are 24-month lookback periods to the vast majority of these. Too many inquiries in the last several months are an indicator of what FICO accounts against your score. FICO keeps a record of and scores against you the last several months, but 24 months’ worth is what’s on your raw data files. The consumer disclosure files that we talked about, you’ll see 24 months’ worth of information and inquiries registered there. Since they only count against your score for twelve, people get deceived or they feel like, “It only counts against me for twelve.” It counts against underwriting and the 24-month lookback period for all 24 months.

Too many inquiries in the last twelve months, too many accounts opened, but remember it’s logarithmic in nature. There’s three months, six months, twelve months and 24 months in that calculation. Notice proportion of balances to credit limits on national revolving accounts is too high and then amounts owed on revolving accounts is too high. Remember a couple of episodes ago when we talked about being fundable and in the underwriting criteria, there was total debt load. That total debt load comes right out of amount owed on revolving accounts which is too high. That’s the measurement that they look at. They filter it through and think of it as red, yellow and green. Red is un-fundable. Yellow is possible if everything else works out and green is off the chain and we accept it.

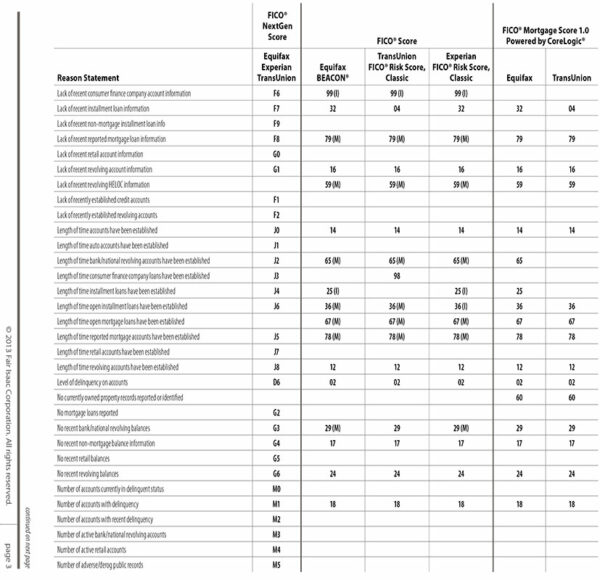

You put enough of those together, whether it’s five in some underwriting categories, seventeen and others and all 40 and others. It is math, but the beauty of math is that two plus two equals four, at least in this universe base ten. It is always universally and absolutely four. We want to look at what proportion of balances to credit limits means utilization. How much of the limit have you utilized? Length of recent banker national revolving information. How long have you had national bank cards? You’re going to be learning in two or three episodes from now where we’re going through those that they’re referring to tier one and some tier two accounts. Tier two banks and value contribution of different cards and all of it. Time says derogatory public record or collection is too short.

If you don't know what's being measured, you're going to be distracted by those shiny objects called credit scores #GetFundable Share on XIt’s three months, six months, twelve months and 24 months. There is a valuation. They all wouldn’t fit here, but this goes to 28-ish. There are 40 that FICO measures and in a separate episode, we are going to be covering the scorecards that FICO uses because there are thirteen scorecards. Thirteen for good or bad credit, five and eight, respectively, for a total of thirteen scorecards, which is where they gather all that information. We’re going to be going through those scorecards and talking about exactly how the lenders use the scorecards to group you as a borrower. People with bankruptcies have a scorecard. People with collections, people with 30-day late but no other things.

There are different scorecards for each one of these, so all 40 of these are grouped together in different ways. Some people ask, “What optimization?” Because many of you are still stuck in that good credit, bad credit. We’re getting away from good credit, bad credit, we’re optimizing, “Are you fundable or not fundable?” What is the essence of optimization? The essence of optimization is where you increase positive fundability™ points. This is not about credit score. All of these that we went through is not about credit score. They’re evaluating your behaviors. Do you have too many inquiries? That’s a behavior. Too many accounts with balances, that’s a behavior. Times with derogatory public record, that was a behavior. How long ago was that negative behavior?

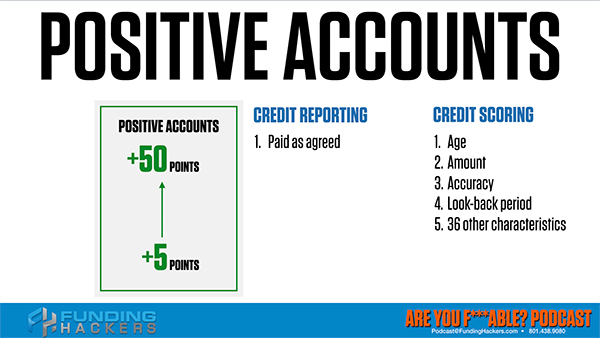

No recent revolving balances, that mean you’re not putting traffic on your card. What kind of traffic are you putting on your card? Every one of these is behavior and they’re counting it for three months, six months, twelve months and 24 months. The essence of optimization is to increase the positive fundability™ points and decrease the negative drag against your profile. Let’s take a look at what that means. First of all, I use the pie chart because what we’re going to discuss doesn’t relate to 50 and 5 for every single client. It’s not absolute. It’s relative to your profile. It depends on the size of your pie, but relatively speaking, a positive account can count 50 points to your score or only five points to your score. What you read is paid as agreed under credit report because all you’re seeing are these three-digit numbers reflected for the different FICO scores, especially if you’re using the myFICO.com advanced credit report.

You see paid as agreed and you’re thinking, “I’ve done my duty,” but there are other criteria on the credit score. There’s age, the amount, the accuracy of the inter bureau reporting, the lookback period plus 36 other characteristics because they measure 40 things. I want to have the big ones up so you can see. Remember when we talked about in the episode where the difference between credit reporting and credit scoring. Two different outfits do it. Two different organizations are in charge of it. Paid as agreed is what you read and then you get a three-digit score and you’re like, “I’ve got a 750 or I got a 680 or an 810.” Credit scoring is contributing 5 or 50 points because of all of this, not just paid as agreed.

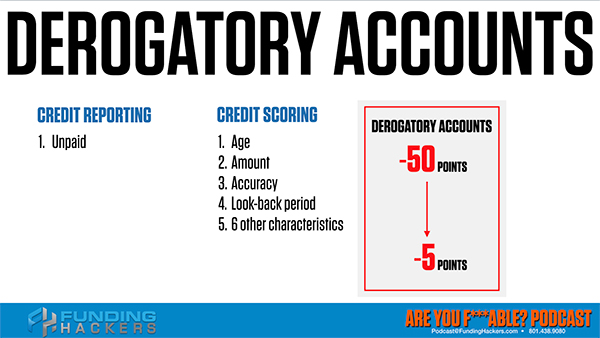

We got to make sure that you understand this because the negative is also true. Let’s say in this instance, it’s all relative to your profile, but let’s say in this instance that a negative account can have 50 points against you or five points against you. That’s why there are significant drop when you have a 30-day late or you get a new collection that you didn’t anticipate or some other financial injury occurs. All of a sudden, your profile is whacked, your score plummets. If you know what you’re doing, if you know how meaningful these different FICO 40 characteristics are, then credit reporting says, “Let’s call it a collection account.” It says unpaid collection and you’re like, “I haven’t paid that collection yet.” FICO is calculating its age, its amount, the accuracy between bureaus, the lookback period and other characteristics.

The ultimate in optimization is to increase the positive yield, the positive points and decrease or lower the negative drag. We want positive account scoring with the maximum number of points possible for your file. We want any derogatory that cannot be legally disputed and removed. We want those counting only five points, the equivalent of, relatively speaking, five points against you. Do you see what I’m saying? If you optimize your positive points, remember what I said, there are 30 ways to improve your fundability™, raise the value of your profile without touching any negative points. If every one of your accounts is raging on amazing profile, amazing point yield on all your positive accounts and you have one or two negative items that have been optimized, but the negative drag has been minimized.

Do you see the power in this? This is why we have clients with 800-plus credit profiles. They’re 810. They don’t have an 850 because they have a few of these, but they’re still fundable because they fall on the grid. The top three or four items of fundability™ are based on making sure you get approved, the 24-month lookback period, etc. Your score dictates the terms, the interest and the amounts. This is optimization. Increase the positive yield on your positive accounts and decrease the negative drag on your negative accounts. This is the essence and everything we talk about in optimization is going to drive this point home more and more. I am thrilled that you are churning through this content.

I know we’ve been doing dozens of these so far. We’re just getting started because we’re laying down the cover fire. We’re laying down the foundation upon which we’re going to address the interviews that I have. We’re bringing on FICO team members, lender underwriters and vice presidents of banks. They are not going to give us their secret sauce per se. They’re going to give us the direction of how all of this automatic underwriting is going to serve when we know the rules of this game, how we can continue to be fundable and validated. We have so many great people that will be coming on board and talking with us as we explore this content. I have so much to share with you. You have so much to discover. Together, we’re going to keep playing this game until we all have our hundreds of thousands in funding or millions of dollars in funding. Until next time.