In this highly technological era, protecting your identity from thefts and annoying sales agents can be a challenge. The good news is, you can actually do so and there are many ways to do it. Merrill Chandler shares some strategies on how to protect your personal credit identity from fraud, being hijacked, and even being stolen. He also touches on techniques to protect your fundability™ that will, in turn, protect your identity. On today’s show, get the lowdown on the ways to protect your identity and make it bulletproof when it comes to identity fraud and theft.

—

Watch the episode here:

Listen to the podcast here:

Protect Your Identity

This episode we’re going to be talking about how to protect your personal credit identity from fraud, being hijacked, even being stolen. We’re going to have an entire lowdown on what the ways to protect your identity are and how to create a singular identity that becomes as bulletproof as it gets when it comes to identity, fraud and theft. This is where the rubber meets the road, especially when it comes to your identity. We are going to be talking about certain little known strategies. These are literal secrets that will protect your fundability™ because it will protect your identity.

One of the first episodes had to do with how important your identity is for creating fundability™ because that identity is the sun around which all of the planets of your accounts revolve. If that sun is not stable, you’re not going to have the gravity that you need to attract lenders who trust you or trust who you say you are when you fill out an application. Be sure to go to GetFundable.com. All of the things we’re talking about are in a module that I give my clients. I’m giving it to you. All you have to do is go in there and tell us where to send it. We’re going to send it to you.

Here is the first thing that we’re going to cover. First of all, there are other consumer disclosures besides the first three we talked about several episodes ago. A consumer disclosure is an official document that you get free once per year from anybody who holds data on you that collects it and holds data. We talked about Experian, TransUnion and Equifax, the three credit bureaus all hold data on you. We’ve shown you how to go to AnnualCreditReport.com and collect that. Get one free report per year. That’s what holds all the data for your 24-month look-back period, etc.

Consumer Disclosures

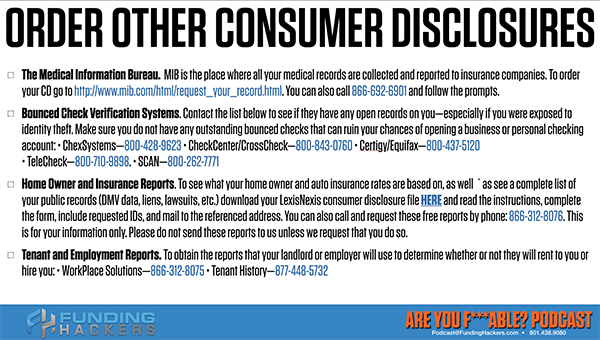

There are other consumer disclosures that are important for you to understand and know because what I tell everybody is you have to have the information before your lenders do. Anybody who’s making a decision about you, you need to know what they know and you need to know it before they know it. Let’s go over some of these. First of all, there’s the Medical Information Bureau and that link is going to be in the PDF that we send you or you’re going to be able to download. You can also call them, but the Medical Information Bureau is the place where all your medical records are collected.

You have a medical transcriptionist and people are collecting all that data and the doctors are writing it down but are the equivalent of stenographers. The people who translate all of those doctor’s instructions, do you know where that stuff ends up? The Medical Information Bureau, it is the warehouse. It is the credit bureau for your medical data. When you are in the FICO, many other insurance providers use the data that’s on the medical information bureau in order to establish your insurance rates. Whether or not you have a preexisting condition because they look at the Medical Information Bureau and if you did a cancer test and it was positive before you got your insurance, they’re going to call it a preexisting condition.

Protecting your fundability™ will protect your identity #GetFundable Share on XIt’s because it’s in the Medical Information Bureau. You need to get your copy of that and find out what’s being reported on you medically. The next one is the bounced check verification system. There are five of them. There’s a very difficult path to getting to the online versions of these. They make it difficult. They are offering it to, as Congress has mandated everybody, you get a free report once per year. The check systems, CrossCheck, Certegy, TeleCheck, all of those you call them and find out what checks may have been written in your name that may stop you from getting further bank accounts. All of the check systems are used for all business banking relationships. If you’ve got something hanging out there, whether it’s yours or somebody did something in your name, you’re going to want to know about it before you get denied that business checking account or otherwise.

When I say somebody has a used a check in your name, I’m going to tell you about ways to protect yourself from those checks. The next one is the homeowner and insurance reports. You are being charged homeowner insurance based on data that is collected in previous insurance claims that you’ve made. Remember when we went over the FICO, there was one of the FICO things that are establishing your tendency to use your homeowner insurance. FICO has a scoring model. FICO uses the data from these insurance reports to score you to see what homeowner rates that you should get. In the disclosure that you’ll download, there are links to be able to go through and get a copy of all of these.

One of those is the LexisNexis Consumer Disclosure. The request form is all downloadable there. I know this stuff is a pain in the ass. I know it. If they’re reporting it, insurance companies, lenders, your employers or your landlords are pulling it, you got to know what that was being reported. You can dispute every one of those. Anything can be disputed if it’s inaccurate, unverifiable or erroneous. If it’s an error, it’s inaccurate or it is unverifiable, they have to remove those items. It’s not the credit bureau that’s disputable.

The last one on this page is tenant and employment reports. This is where workplace solutions, tenant history, these are the places where employers pull files to determine whether or not they’re going to hire you or what your financial tendencies happen to be. If you’re in tons of debt, people have been denied employment because they’re overwhelmed in debt. You’ve got to find out what’s being offered. Those credit reports, those employment reports, the tenant reports are all being, are all being marketed to and offered to landlords and employers everywhere. Find out what it says. We’ve got to know so that you can take actions about it. We’re not going to go through every single one of these, but this list will be in your download.

Pay Your Bills Via Phone Or Online Secure Bill Paying Systems

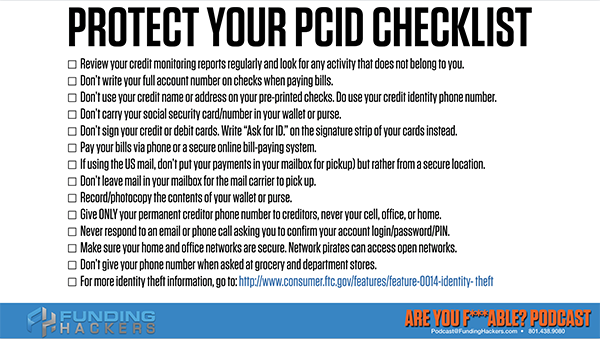

One of the things that you need to understand, I want to jump down to it is don’t carry your Social Security card or your number in your wallet or purse. Many people keep their actual Social Security number in there. Here’s the other thing. You don’t want to have your credit name, your PCID. You don’t want your PCID or your PCID address on your preprinted checks. That’s giving away the information to steal. You want to pay your bills via phone or secure online bill-paying systems. If you’re using a US mail, don’t put your payments in your mailbox for pickup, rather use a secure location.

You're more fundable when you're not susceptible to lenders #GetFundable Share on XMainly the postal workers call the big blue monsters, dropping it in there or taking it to a UPS store or otherwise so it can be mailed. Don’t leave mail in your mailbox for the carrier to pick it up. Here’s what’s happened. When you flip up that red notification that says, “I’ve got mail in here,” you’re broadcasting to any nefarious person, anybody who’s looking, driving neighborhoods that are looking for mail. You’re telling them, “Come on by and sort through my mail and see if there are any goodies that you can use.” Try it at home, if you sign a check, many of us don’t use checks anymore, especially old-schoolers and especially Baby Boomers.

The Baby Boomers are the ones who have spent decades now building their careers, have assets, wealth and money. Our generation, we use checks. If you’re old school and you’re using checks, be aware of this. If you sign a check, you fill it out and you’re going to pay a bill with it, do you realize that’s somebody who knows what they’re doing? You’re going to know because I’m going to tell you, you can take that check. You can dip it into acetone and don’t get it wet where the signature is, it will melt all of the ink off. It will completely dissolve the ink except for where your signature is. Anybody once that acetone dries, you’re able to fill out the check to any amount and with a bonafide signature on it.

Don’t Sign Your Credit Or Debit Card

When that signature is there, it passes muster and you have to fight with the bank saying, “I didn’t make this check.” They say, “This signature matches your signature on file at the bank.” Do not use checks to pay your bills. Pay bills via phone or secure online bill-paying service. The final thing, read through them all. Do them all. Somebody who knows what they’re doing, how they can take it advantage. The other thing is don’t sign your credit or debit cards right where it says for signature, write ask for ID. Many merchants and vendors ask for ID already, but you should write, “Ask for ID,” on the back of every single one of your credit cards and your debit cards so that way they’re matching your name and your information. Go through this. Here’s the issue.

You can make a bulletproof personal credit identity when you are able to get as close as possible. It took me several years to get one name, one address, one phone number, one set of employers and one Social Security and date of birth on my profile. Some accounts were linked or some were hanging on. Some of the bureaus wouldn’t let go of a couple of the data points. If you apply with only one like Merrill R. Chandler. Let’s say that that’s my PCID name Merrill R. Chandler. If my driver’s license says Merrill Ray Chandler and somebody steals my wallet and tries to take that information and put on an application Merrill Ray Chandler because that’s what my official documentation says. Every creditor on the planet has Merrill R. Chandler, they’re going to get denied because of the data points.

We’re going to continue talking about this more, but the data points don’t match up. That application is going to be denied because the fraud software, FICO, Falcon, early warning systems and the credit bureau databases are all going to have the same message, Merrill R. Chandler. I’m not telling you all that I do. I’m using that as an example. The better, more clear and more singular your identity, the better opportunity you have of having a clean and clear personal credit identity. The better your funding are going to be because they don’t even get to whether or not they want to fund you, if they don’t trust the data points that you’re putting on the application. Make sure that you clean up your personal credit identity as we’ve done on one of the early episodes.

If you're looking to become a truly professional borrower, remove yourself from every possible mailing list as you can #GetFundable Share on XDon’t Respond To Credit Offers

Make sure you get that done. If you want help in that, go to the bootcamp and it’s one of the things we do in the bootcamp, GetFundableBootcamp.com, you’re set. Get these done, follow these instructions and you have the much higher likelihood of surviving in this identity theft world. Let’s talk about another way to protect your fundability™ in big screaming letters. I’m saying do not respond to credit offers. People say, “Why sometimes those offers are awesome?” I’m like, “I didn’t say don’t get a new credit card or credit line.” What I’m saying is don’t respond to credit offers because the fundability™ of your profile falls into two categories. Are you a proactive borrower, read professional borrow? Are you a reactive borrower? Are you a consumer? Are you an amateur? Are you a rookie?

That’s my language. The proactive borrow versus a reactive borrower, they grade you on your susceptibility to credit offers. Why? If all you have to do is sit at home and receive an email or a letter and it says, “We’ve got this great little opportunity for you to get a credit card, you sit there and you fill it out and there are a dozen different names for it. There’s a promotion code or the activation code or offer code, any of those names or 100 different other ones, a dozen different other ones. You put it in code, you are ending up on a marketing list that says this person responds to offers. Sitting on your bank, has a window popped up in one of your credit card or banking apps that says, “Would you like better credit card offers or better offers from us? Give us your income.”

What they’re doing is they’re collecting data points to compare later so that fraud software can detect. If you’re logged in and you’ve passed muster on a particular account, chances are you’re the authorized user of that account. You’re the owner of the account. When you’re in there and you put in your income there, that goes into Falcon and other databases to verify so they can check. Let’s say it’s a $6,000 a month and somebody says, “I make $7,000 a month,” filing an application in your name, they’re going to get denied because the tolerance of $6,000 to $7,000 may be too much over certain period of time. Those time periods are 3 months, 6 months, 12 months and 24 months. The tolerance is FICO did not answer our questions about what the tolerances were, but if it’s too far out of those tolerances, that applications are going to get denied.

They’re asking for this information intentionally on your banking websites. We want to be a proactive borrower, not a reactive. The other thing I want to say is if you like an offer, don’t respond to the mail or the email, go to the bank, call the 800-number or whatever it is. Don’t do any of this until you do the episode where we’re talking about the quality of your accounts. I’m going to tell you what types of accounts are high-value and which are low-value. Don’t do anything until you do that episode. If you like the offer, don’t respond. Don’t put it in a code. Contact the credit card issuer, the lender and say, “I would like to have this blank card.”

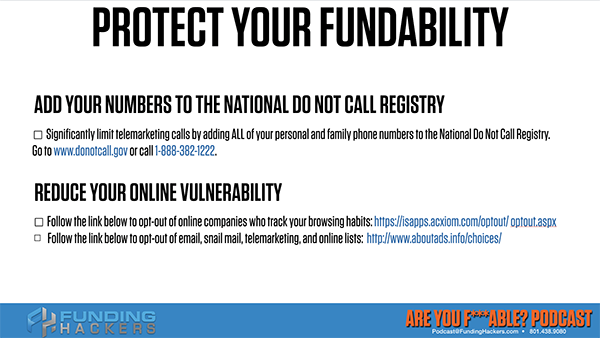

You’ll still get the same rates and terms. Confirm and say, “What’s the rate and term? How much interest are you going to charge me?” Use the offer to get the same offer, but don’t put in the code because the second you put in the code, you’re verifying yourself as an unsophisticated borrower susceptible to lending. Let’s take that one step further. What about if you already have, again, you need to go to OptOutPreScreen.com. This is where all the credit bureaus have consolidated. Ordering a consumer disclosure is one website representing all the bureaus, OptOutPreScreen.com will remove your name off of the credit bureau mailing lists where these offers are coming from.

We have found anecdotal evidence from our clients when they remove their name from these credit bureau mailing lists or the offer lists, their scores have gone up ten to twenty points. The question is why? Why would somebody score go off getting off of these databases? If you connect the dots, it’s simple. They’re raising your score because you’re now more fundable because you’re not susceptible to lenders. Let’s say Chase sent you an offer. You fill out the offer from Chase. You put in the code and you get approved. The next person is going to look and say, “There’s a recent inquiry.” I don’t know if they were approved or not, because in that 30-day period, even if you’re approved, it doesn’t show up on your credit report for one or maybe two reporting cycles.

Opt Out And Remove Yourself From Every Mailing List

They don’t know that you’ve been approved. They may deny you because of the inquiry or the 5-24 rule. If there are more than five approvals in 24 months, you’re going to get denied on the 6th, 7th, 8th, 9th and 40th after that. Doing the OptOutPreScreen.com removes you from the list so you’re not susceptible. Any new lenders that are coming after a current lender are not afraid. They’re like, “I don’t know what they’ve been approved for other places. I’m not going to approve them. It’s a valuable tool. Make sure you implement it. Here’s the other thing that you may have done this before but go to your My FICO Credit Report if you haven’t pulled it. MyFICO.com get the credit monitoring and you need to opt-out of every version of your name. They’ve been collecting this stuff for a reason. You’ve been putting it up because you didn’t know better. They didn’t teach you.

They didn’t reveal the truth of the funding game. They’ve kept you in the dark. We’re now learning this for the first time. In your case, when you opt-out, you need to opt-out of every single version of your name and out of every single address that is on the credit report. Even if you don’t live there, it takes a minute because mail forwarding, do not forward address correction requested. There’s a whole bunch of United States Postal Service Mechanism for updating addresses for people who are inquiring. Opt-out of every version of your name and every address so that you can have the most confidence that you’re as impermeable and bulletproof as possible.

Opt-out each version of your name and each address listed by each of the credit bureaus. You’ve got to make sure you do that. If in any of these exercises, any of the episodes, if I say this is a red dot activity, let me tell you what that means. This is what red dot means. I took a personal development training years ago and we all had our name tags so that the facilitator could work with us. The facilitator said, “When it’s your turn, if I’m processing you, if we’re doing an exercise, if I’m speaking to your accountability and making sure that you’re getting the most value out of this training, if you want me to go all the way, if you don’t want me to pull punches, if you want me to knock it out of the park with you, why don’t you go to the back table, get a red sticker and put it on your name tag?”

That’s the red dot. Red dot activities mean that you want to go all the way. You’re going to push the envelope. Some people argue, my team argues that every single thing I ever talked to you about is a red dot activity. I may separate it out as the urgent and important versus the important but maybe not urgent. These are red dot activities. If you opt-out from the national, regional, local marketing and mailing lists, first of all, you significantly reduce your impact on the environment, the number of trees you saved. If the environment is important to you, these are madly important ways in which you can contribute. When it comes to your financial well-being and your financial life, every one of these links in these phone numbers will remove you from mailing lists. I’ve talked about it before, but we need to understand that your magnetic stripe on each of your credit cards or debit cards, you’re sending your information to that store.

When you swipe it, you’re linking the SKUs. The SKUs for each of the items you have purchased. They’re collecting that data when you swipe that card. If you pay for cash, nobody is collecting any data. If you’re swiping your card to pay for it or putting in your chip to pay for it, they are logging your information there. They’re limited on the information. It’s not that your name, address, phone number, Social Security, none of that. What their logging is your contact information and your pertinent demographics. They’re logging that to those purchases. Have you ever purchased something online, bought a nice watch or whatever? All of a sudden you started getting mail from nice watch companies or from purveyors of fine watches. It happens all the time. You told that merchant, I am susceptible to watch purchases and you will start getting marketed to.

That puts us still on the amateur and rookie. You can keep anything you want. I know people who love junk mail. They want to see what’s out there in the world. They love coupons. Don’t do what I’m telling you. If you’re looking to be truly a professional borrower, professional in the financial realm, remove yourself from every possible mailing list you can. I’ve gotten myself so far out of the junk email lists and everything that when I do receive one, I get Uline’s all the time, Uline catalogs. I’ve called them up three different times. They keep sending it to the resident. I have to take residents out of the database and off their mailing list because that is a mad waste of paper and I’ve never bought anything from Uline in my life.

While I may be off the charts in my priorities and proclivities, I’m giving you the tools to knock it off to get out of the being a passive recipient of all the marketing out there, be a deliberate and intentional buyer. Don’t be at the effect of the market, be at cause of the market. There’s that one. Another couple of very important ones. Make sure you add your numbers to the National Do Not Call Registry. You can go online DoNotCall.gov or call them and you can put in on the phone in an automated fashion. You want every single number, your children’s numbers, your numbers, your home number, work number, all numbers.

I’m going to give you a little hint. Unless it says Scam Likely if you’re receiving these types of things, Scam Likely may not respond to this, but legitimate telemarketing outfits who are obeying the law. If the second they answer start their pitch, whatever their pitch is, if you hit number two once or sometimes twice, you will be put on the do not call registry for that outfit. You don’t even have to listen to the pitch. Trigger the automatic attendant and when they start talking, hit 22 twice. The legitimate telemarketers will take you off the do not call registry. There’s that one.

Finally, the last one is reducing your online vulnerability. You can opt-out of online companies who track your browsing habits. You can always go private windows are dark but get rid of the records of your browsing habits. Also opt-out of the email, snail mail and telemarketing list by going to about ads. I want you to be at cause not at effect of these marketers. Protect your fundability™. I want in every possible way to make sure that you guys are protected safe and that your borrowing habits are being measured. You’re giving FICO and the lender software the best possible opportunity to grade you high so that you can have the funding opportunities that you deserve to grow your life, grow your businesses. We will see you in the next episode of The Get Fundable! Podcast because I definitely want you to be.

Important Links:

- AnnualCreditReport.com

- LexisNexis Consumer Disclosure

- OptOutPreScreen.com

- MyFICO.com

- DoNotCall.gov

- GetFundable.com